(909) 217-7855

Call us for a consultation

Picture this scenario: You’ve just wrapped up your company’s financial year, and a lender or potential investor requests to see your financial statements. Should you provide a reviewed statement or an audited one? And what’s the real difference between the two? If you feel unsure, you’re not alone. While both Reviews and Audits involve the expertise of a Certified Public Accountant (CPA), each offers a different level of assurance, employs different procedures, and comes with a distinct cost structure.

Below, you’ll discover how Reviews differ from Audits and how to determine which service is right for your business.

Both Reviews and Audits are considered “attest engagements,” meaning a CPA provides an opinion or conclusion on financial statements. However, they fall at different points on the assurance spectrum:

In a Review engagement, the CPA primarily uses analytical procedures (like ratio or trend analysis) and makes inquiries (asking management targeted questions). The result is a limited assurance conclusion, often phrased as: “We are not aware of any material modifications.

An Audit goes deeper. It involves extensive testing, verification of transactions, confirmations from external parties (such as banks and vendors), and a thorough evaluation of the company’s internal controls. This level of scrutiny provides reasonable assurance that your financials are free of material misstatement—the closest you can get to a professional “seal of approval.

When it comes to financial reporting, business owners often need to choose between a Review and an Audit of their financial statements. While both involve the expertise of a CPA, they differ in terms of level of assurance, depth of analysis, cost, and regulatory requirements. Below is a detailed comparison to help you understand which option best suits your business needs.

| Criteria | Review | Audit |

| Level of Assurance | Limited assurance | Reasonable assurance |

| Procedures Involved | Analytical procedures and management inquiries | Substantive testing, external confirmations, and transaction verification |

| Depth of Analysis | Less detailed, focuses on plausibility | Thorough examination of financial statements and controls |

| Cost | Lower cost due to limited testing | Higher cost due to extensive testing and verification |

| Time Required | Quicker process, typically a few weeks | More time-intensive, taking weeks to months |

| Staff Involvement | Minimal disruption to staff | Greater involvement, requiring staff cooperation |

| Regulatory Requirement | Not required by law for most private companies | Required for publicly traded companies and certain regulated industries |

| Ideal For | Small businesses, startups, or firms without audit mandates | Companies seeking major financing, mergers, or regulatory compliance |

| Investor/Lender Acceptance | Often acceptable unless an audit is specifically required | Preferred or required for large transactions or high-risk industries |

| Internal Control Evaluation | Not a primary focus, only reviewed at a high level | Includes detailed assessment of internal controls |

| Documentation Requirements | Limited documentation needed | Extensive documentation and supporting evidence required |

| Detection of Fraud/Error | Lower likelihood of detecting fraud or material misstatements | Higher likelihood of detecting fraud or material misstatements |

| Management Letter with Recommendations | Not typically included, unless requested | Often included with insights on internal controls and improvements |

This comparison chart can help you decide which engagement aligns with your business needs and compliance requirements.

Understanding the scope and procedures of financial reviews and audits is essential for assessing their purpose and reliability. While both provide insights into financial statements, they differ in depth, methodology, and level of assurance.

Reviews are cost-effective with minimal disruption, ideal for smaller entities. Audits require more time, higher fees, and deeper staff involvement due to extensive testing and documentation.

A review is suitable when limited assurance meets lender or investor requirements, for smaller businesses needing a basic financial check, or when management seeks an external perspective without the depth of an audit.

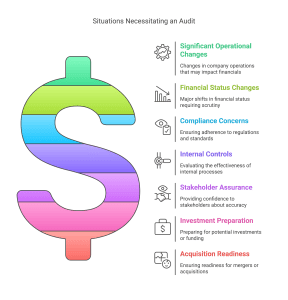

An audit is recommended for regulatory compliance, major transactions like mergers or financing, and high-risk or complex environments where deeper scrutiny is necessary.

Choosing between a Review and an Audit depends on stakeholder requirements, budget, internal controls, and long-term goals. If cost and time are constraints, a Review may suffice, while an Audit is beneficial for regulatory needs and future growth planning.

Deciding between a Review and an Audit comes down to balancing the level of assurance needed against cost and complexity. If you only need limited assurance, a Review is often faster and more budget-friendly—ideal for many privately held or smaller companies. However, if strict regulations, large-scale financing, or mergers and acquisitions are on your horizon, an Audit offers the depth and credibility you may require.

Still unsure which engagement fits your situation best? Contact G&S Accountancy for a quick consultation. Our experienced team will help you determine whether a Review or an Audit aligns with your budget, reporting obligations, and long-term objectives. Get in touch today and give your stakeholders confidence in your financial story.

Audits provide reasonable—not absolute—assurance. While more rigorous than Reviews, they can’t guarantee detection of every error or fraudulent activity.

Yes. Many businesses start with Reviews and upgrade to Audits as they grow. A prior Review often helps you organize records and get comfortable working with a CPA.

Often, yes. If a lender or investor only requires a Review, it typically meets their needs and establishes a base level of credibility. Always confirm stakeholder expectations before deciding.

No. Audits generally involve more extensive documentation, testing, and verification procedures than Reviews, which focus on analytical procedures and inquiries.

If you anticipate major deals, investor inflows, or regulatory requirements, an Audit may be the better long-term choice. It provides deeper assurance and can help build credibility for future expansion.

We will happily offer you a free consultation to determine how we can best serve you.

Contact Us Today