(909) 217-7855

Call us for a consultation

Set up your U.S. company + IC-DISC to lower export taxes - without tripping compliance

We structure and maintain a compliant U.S. corporation and an IC-DISC for mid-market exporters and foreign-owned groups—cutting federal tax on export profits, clarifying intercompany pricing, and reducing state-level friction.

- Peer-reviewed CPA firm (Pass)

- Led U.S. first-year financial reviews enabling $50M+ credit lines

- California IC-DISC + owner treatment expertise

- On-time IC-DISC filings (Form 1120-IC-DISC; no extensions allowed)

Problems we Solve

Problem

New start-ups forming their first non-profit.

- Margins squeezed by tariffs, freight, and pricing pressure.

- Confusion about Form 5472, transfer pricing, and California tax treatment.

- Worry about missing IC‑DISC election or filing deadlines.

- BOI rules changed in 2025 - you’re not sure what applies now.

Outcome

After working with us

- Clean U.S. structure with a compliant IC‑DISC supporting export‑profit planning.

- Documented, IRS‑approved pricing method (4% gross receipts, 50/50 CTI, or $482).

- California treatment clarified, including $800 minimum franchise tax.

- Filing calendar that hits every date: 4876‑A election, 1120‑IC‑DISC, 5472 reporting

Our Solution

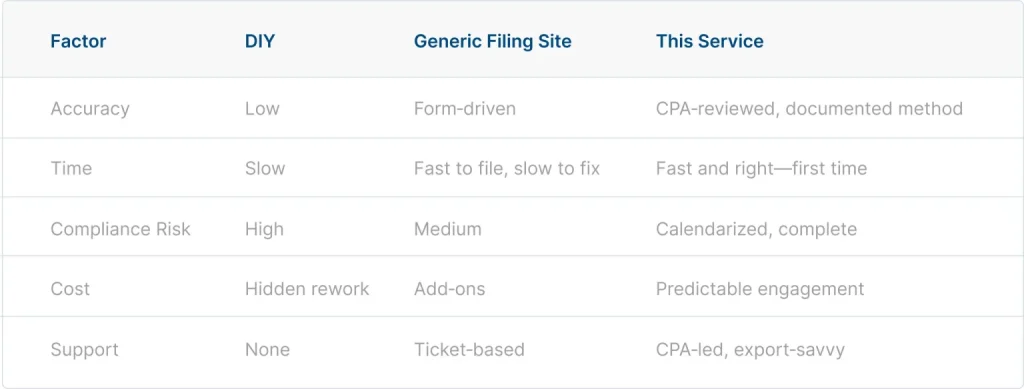

We help exporters and foreign‑owned groups set up a U.S. company and an IC‑DISC the right way. An IC‑DISC is a special U.S. corporation that isn’t taxed at the federal level. Instead, its shareholders are taxed when income is distributed—sometimes with a small interest charge if deferred.

To qualify, the IC‑DISC must meet strict requirements: at least 95% export receipts and 95% export assets, one class of stock worth at least $2,500, and separate books. We guide you through transfer‑pricing choices (4% of export receipts, 50/50 of combined taxable income, or $482), structure the commission funding, and handle all required filings. From day one, we build a compliance calendar so you never miss deadlines and avoid costly penalties.

Scope & Deliverables

U.S. entity selection and formation (with California considerations)

IC-DISC eligibility review (95/95 tests, stock, separate books)

Form 4876-A election package with shareholder consents

Commission calculation workbook (4% vs 50/50 vs $482)

Annual Form 1120-IC-DISC filing + shareholder statements

5472 readiness for 25%+ foreign ownership

California allocation guidance and minimum franchise tax planning.

Filing calendar + audit-ready documentation.

Engagement tiers (custom quotes)

Basic

Eligibility review + 4876‑A election + first 1120‑IC‑DISC

Standard

Basic + commission model + California treatment memo (for $5M–$50M exporters)

Plus

Standard + 5472 package + intercompany agreements + audit support (for >$50M or foreign‑owned groups)

Proof & Credibility

Manufacturer reduced federal tax on export profit by ~15–20%

Foreign‑owned group avoided penalties with proactive 5472 filing

California exporter minimized double counting using FTB 2015‑02

California exporter minimized double counting using FTB 2015‑02

Frequently Asked Questions

What documents will CDTFA ask for?

Sales journals, exemption certificates, bank statements, POS data, purchase invoices, and shipping docs.

How long does the audit take?

Most audits last 3–12 months, depending on scope, records, and CDTFA’s requests.

What if exempt sales/support is missing?

We help reconstruct or organize what you have and address sampling requests.

Can penalties be reduced?

Yes, penalty abatement may be available where CDTFA rules allow.

What if we disagree with the auditor?

We can pursue appeals and payment plans where eligible.

Do you help with payment plans?

Yes, we assist in negotiating manageable payment arrangements when needed.

Location & Service Area

We serve clients locally in Rancho Cucamonga, Ontario, Fontana, Riverside, and San Bernardino, and across Orange County and Los Angeles. Remote delivery is available nationwide and for foreign parent companies.

Download the Lender Checklist and Book a 15-Minute Call to Lock Your Review Dates

Ready to cut export taxes—with clean compliance?