(909) 217-7855

Call us for a consultation

The federal excise tax on trucks is a critical tax imposed on the sale of certain heavy vehicles in the United States. This tax, governed by Internal Revenue Code (IRC) Section 4051, applies to the first retail sale of heavy trucks, tractors, and trailers. Businesses involved in manufacturing, selling, or importing these vehicles must understand the tax’s implications, exemptions, and compliance requirements to avoid penalties and ensure proper filing.

The federal excise tax on trucks is a one-time 12% tax imposed on the first retail sale of specific heavy vehicles, including:

The seller is responsible for collecting the federal excise tax on trucks and remitting it to the IRS, while the buyer bears the cost. Businesses that fail to comply with FET regulations risk penalties, interest, and back taxes.

The federal excise tax on trucks applies in the following situations:

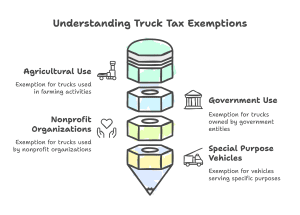

Certain vehicles and transactions are exempt from federal excise tax on trucks under IRC Section 4053, including:

The IRS strictly regulates the application of federal excise tax on trucks for imported used vehicles. If a truck was exported before being sold at retail in the U.S., its first sale or use upon re-importation triggers FET liability.

However, if the importer can prove that FET was already paid before export, they may avoid paying the tax again. To substantiate prior payment, businesses should provide:

Without sufficient evidence, the IRS will likely assess the federal excise tax on trucks upon re-entry.

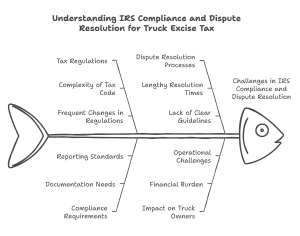

The IRS monitors federal excise tax on trucks compliance through audits and investigations, particularly targeting companies that:

If a business disagrees with an IRS assessment, it can:

The federal excise tax on trucks significantly impacts the heavy trucking and transportation industries. Understanding its regulations, exemptions, and compliance requirements is essential for businesses involved in the sale, import, or use of heavy trucks. Proper record-keeping and tax planning can help companies avoid penalties and audits.

At G&S Accountancy, we specialize in helping trucking businesses navigate complex tax regulations, ensure FET compliance, and maximize tax savings. Whether you need guidance on exemptions, IRS dispute resolution, or strategic tax planning, our expert team is here to assist you.

Contact G&S Accountancy today to schedule a consultation and ensure your trucking business stays IRS-compliant and financially optimized!

The seller (dealer or manufacturer) is responsible for collecting the tax and remitting it to the IRS. However, the buyer ultimately bears the cost since it is included in the vehicle’s price.

No. Only trucks with a gross vehicle weight (GVW) rating over 33,000 pounds, truck-tractors over 19,500 pounds, and trailers exceeding 26,000 pounds are subject to FET. Lighter trucks and vehicles designed for non-transportation purposes are exempt.

To claim an exemption, businesses must provide proper documentation, such as proof of government use, nonprofit status, export records, or vehicle classification as mobile machinery.

If a previously exempt truck is modified (e.g., by adding heavy equipment or changing its purpose), it may become subject to FET. Businesses should consult a tax professional before making modifications.

Failure to collect, report, or pay FET can result in significant penalties, including:

We will happily offer you a free consultation to determine how we can best serve you.

Contact Us Today