(909) 217-7855

Call us for a consultation

If you’re a business owner who’s had a banner year, first of all, congratulations! But as the year comes to a close, you might find yourself dreading a massive tax bill. Let’s take an example: a $1 million taxable income. That sounds like a one-way ticket to a six-figure tax payment, right? However, there are legal strategies that can help you legally avoid paying taxes on that income.

Not so fast. What if I told you there are strategies in the tax code that could legally reduce that liability significantly—even to the point where you might not owe much at all? It sounds impossible, but it isn’t. Here’s how.

Imagine this: You’re a small business owner, and your company generated $1 million in income this year. You’ve worked tirelessly, taken risks, and now you’re staring down a potential $300,000 or more tax bill. Most people in this position would accept the hit as inevitable.

But smart business owners know that taxes aren’t just about paying your share—they’re about using the tools available to minimize your share. Here are four strategies that can make an enormous impact.

The IRS allows cash-basis taxpayers to deduct expenses in the year they’re paid. That means you can prepay certain expenses for 2025 before December 31, 2024, and claim those deductions this year. Examples include:

By accelerating these expenses, you could immediately lower your taxable income by tens of thousands of dollars.

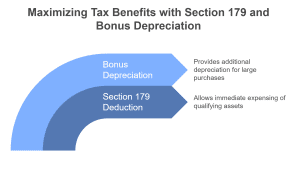

Did you buy equipment, vehicles, or machinery for your business this year? If not, now might be the perfect time. The IRS allows you to deduct up to $1.16 million in qualifying equipment purchases under Section 179 for 2024.

Even better, bonus depreciation lets you deduct 100% of the cost of qualifying assets in the year they’re placed in service. For example:

These deductions can drastically reduce your taxable income while letting your business benefit from new resources.

This is a game-changer for business owners. Setting up or contributing to a retirement plan allows you to not only save for the future but also significantly reduce this year’s tax burden. For example:

These contributions are fully deductible, turning your retirement savings into immediate tax savings.

If you’re a sole proprietor or run a small business, hiring your children under 18 can be a highly effective way to lower your tax burden. Here’s why:

Not only does this help with taxes, but it also allows you to put money into their future—perhaps through a Roth IRA or college savings fund.

Let’s put it all together. Here’s how these strategies could work for a $1 million business income:

That’s $460,000 in deductions—cutting taxable income nearly in half. Combine this with other credits and advanced planning, and your total tax liability could shrink dramatically.

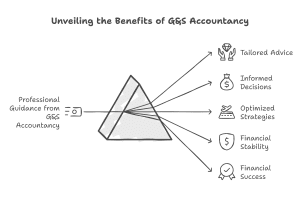

While these strategies are legal and effective, implementing them correctly requires expertise. Missteps can lead to missed opportunities—or worse, IRS audits. That’s where we come in. At G&S Accountancy, we specialize in helping business owners navigate complex tax situations, ensuring they maximize savings while staying compliant.

The clock is ticking—these strategies are only available if you act before December 31. The good news? You don’t have to figure it out on your own. Schedule a consultation with us today, and let’s make sure your hard-earned income stays where it belongs: with you.

We will happily offer you a free consultation to determine how we can best serve you.

Contact Us Today