Use Reviewed Financials to Negotiate Better Lending Terms — Here’s How You Do It

If you’re aiming to fuel growth—whether by stocking inventory, purchasing new equipment, or funding a strategic expansion—you’ll likely turn to a line of credit or a term loan. Yet many owners like you leave money on the table because lenders don’t fully trust internally prepared numbers. That’s where reviewed financials come in. When a CPA issues a review, you deliver limited assurance that’s far more persuasive than a bare-bones compilation yet far less costly than a full audit. The payoff for you? Lower interest rates, higher credit limits, and looser covenants.

How Your Bank Prices Risk

Before any loan officer quotes a rate, the bank ranks you on two dimensions that together determine your cost of capital.

- Financial strength – profitability, leverage, and cash-flow coverage

- Reliability of the numbers – the higher the assurance level, the lower the default uncertainty

| Statement Type | Assurance Level | Typical Risk Premium |

| Internally prepared | None | Highest |

| Compiled by CPA | No assurance (format only) | High |

| Reviewed by CPA | Limited assurance | Moderate |

| Audited | Reasonable assurance | Lowest |

Key takeaway: Upgrading from a compilation to reviewed financials often trims 25–75 bps from your rate or boosts your credit limit by 10–20 % (2024 Mid-Market Lending Survey, ABL Analytics).

Why Reviewed Financials Win Over Credit Committees

Every loan file passes multiple layers of scrutiny, and reviewed statements give you a leg up at each stage.

- Independent validation. During a review, your CPA runs analytical procedures and probing inquiries. When they conclude “nothing came to our attention indicating material misstatement,” the bank knows an objective professional has stress-tested your numbers.

- Early-warning insights. Those same analytical procedures uncover unusual trends early, giving you time to fix issues before an underwriter flags them.

- Stronger covenant negotiations. Limited assurance boosts confidence in your ratios, allowing you to push for softer leverage, liquidity, and debt-service covenants.

Real-World Payoff: A Quick Case Study

One client’s experience shows how reviewed financials translate directly into savings.

Company: Pacific Components (Manufacturer, $12 M revenue)

Need: Refinance a 9.25 % equipment loan and expand a working-capital line

Action: Engaged G&S Accountancy Inc. for first-time reviewed financials

Result: Rate dropped to 7.6 %, credit line grew from $500 k to $750 k, and the personal guarantee disappeared—largely because the review reduced perceived risk.

Annual savings: $32 k in interest

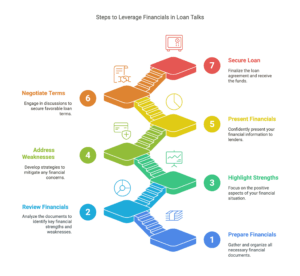

Five Steps to Leverage Reviewed Financials in Your Loan Talks

Use this short roadmap to convert your upgraded statements into concrete pricing and covenant wins.

- Schedule the review early. Wrap fieldwork at least 60 days before renewal so last-minute pressure doesn’t erode negotiating power.

- Spotlight key ratios in a cover letter. Tie debt-service coverage, EBITDA margins, and leverage ratios directly to the reviewed report so bankers can trace every figure.

- Pair reviewed historicals with projections. A 12-month forecast underscores your future repayment capacity.

- Request pricing grids. Ask how each risk-grade notch translates into rate reductions, then negotiate based on your upgraded assurance level.

- Invite your CPA to the call. Having an independent expert live on the line speeds approvals and answers technical questions instantly.

Conclusion

Think of reviewed financials as a credit-worthiness amplifier—bridging the gap between unaudited statements and a full audit. When lenders see limited assurance from a trusted CPA, they’re more inclined to extend lower rates, larger limits, and friendlier covenants.

Ready to bring reviewed statements to your next loan negotiation? Contact G&S Accountancy Inc. or email us at info@gns-cpas.com. Our team delivers cost-effective reviews that convert directly into financing wins.

Frequently Asked Questions

Will every bank cut my rate just because I have reviewed financials?

Not automatically—but most community and regional banks apply lower risk premiums to limited-assurance statements than to compilations or internal numbers.

Is the extra fee over a compilation worth it?

If your rate savings exceed the review cost (typically $5–15 k for mid-size firms), the math—and the added credibility—work in your favor.

Can the same CPA who files my taxes handle the review?

Yes, provided independence rules are met. Your CPA simply can’t hold a managerial bookkeeping role for you.