Are Your Internal Controls Holding You Back?

When you hear the term internal controls, you might picture a large corporate finance team poring over detailed checklists and formal policies. However, internal controls are just as vital for small and mid-sized businesses. These systems are designed to safeguard your financial data, prevent fraud, and ensure operational efficiency.

During a review engagement, where an independent CPA provides limited assurance on your financial statements, underlying issues with internal controls often surface. While reviews don’t involve the comprehensive testing of an audit, they can still highlight red flags and weaknesses in your financial systems.

In this article, we’ll explore why internal controls matter, how review engagements help identify weaknesses, and practical steps to strengthen your internal control framework.

Why Internal Controls Matter?

Implementing strong internal controls helps businesses achieve operational stability, maintain accurate financial reporting, and reduce exposure to risk. Whether you’re a startup or an established company, these controls provide the structure your business needs to function efficiently and ethically.

Below are key reasons why internal controls are essential for any organization:

- Minimize the Risk of Fraud: Segregating duties, enforcing approval protocols, and conducting regular reconciliations create a reliable system of checks and balances.

- Enhance Financial Accuracy: Effective internal controls reduce errors such as double entries, missing invoices, or incorrect classifications by catching them early.

- Build Stakeholder Trust: Transparent financial practices reassure lenders, investors, and business partners that your business is accountable and well-managed.

- Improve Operational Efficiency: Streamlined processes and fewer errors allow your team to focus on higher-value tasks rather than troubleshooting issues.

Where Review Engagements Reveal Weaknesses?

While a review engagement doesn’t test internal controls directly like an audit, it still involves analytical procedures and inquiries of management that can expose potential issues. These review activities often uncover inconsistencies or patterns that point to internal control weaknesses.

Common control issues that can surface during a review include:

- Unexplained Variances: Sudden spikes in cost of goods sold or other financial discrepancies may indicate process breakdowns, such as poor inventory control or unapproved spending.

- Unusual Journal Entries: Large, last-minute entries could point to errors, oversight, or rushed efforts to balance the books.

- Overdependence on a Single Employee: Relying on one person for multiple key accounting functions—like payroll, payables, and reconciliations—raises significant internal control concerns.

Although not the primary goal, a review engagement frequently highlights these vulnerabilities, prompting businesses to evaluate and improve their internal controls.

Common Internal Control Pitfalls and How to Fix Them

Many organizations struggle with similar internal control issues. Recognizing these common pitfalls is the first step to addressing them effectively. Below, we outline frequent weaknesses in internal controls and offer practical strategies to resolve them.

-

No Segregation of Duties

- Issue: One individual handles disbursements, bank reconciliations, and accounting entries.

- Solution: While full separation may not be feasible in smaller businesses, periodic oversight by a manager or owner can help mitigate this risk.

-

Incomplete Documentation

- Issue: Transactions lack supporting documents, making it hard to trace sales, expenses, or receipts.

- Solution: Require consistent documentation and reconcile accounts regularly to maintain accuracy and transparency.

-

Weak Approval Protocols

- Issue: Purchases and payments are made without formal approval, increasing the chance of error or misuse.

- Solution: Set clear rules for approving expenditures, and document all authorizations, whether digitally or in writing.

-

Limited Review of Financial Reports

- Issue: Financial reports go unchecked outside the accounting department, allowing errors to persist.

- Solution: Ensure that management regularly reviews financial summaries and investigates unusual fluctuations.

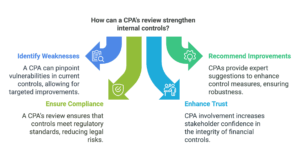

How a CPA’s Review Can Strengthen Internal Controls?

Although a review engagement is limited in scope, it offers several benefits when it comes to identifying and improving internal controls. A CPA’s perspective often brings attention to areas where better controls could enhance financial accuracy and reduce risk.

Here’s how a CPA review indirectly supports internal control improvements:

-

Encourages Accountability

The expectation of external review encourages your team to follow internal procedures and maintain cleaner records.

-

Highlights Operational Red Flags

Analytical comparisons and trend analyses often point to patterns that may stem from control weaknesses—such as frequent journal entries or erratic expenses.

-

Provides Informal Recommendations

CPAs may suggest practical control enhancements even during a limited review, such as increasing oversight or improving documentation.

Real-World Lessons from Review Engagements

Review engagements often bring to light recurring control challenges that businesses may have overlooked. These findings offer valuable insights for improving internal processes and minimizing future risk.

Here are a few examples of what businesses often learn through review engagements:

-

Recurring Financial Discrepancies

If your financials require frequent corrections, it’s likely a sign of weak internal controls—implementing tighter invoice matching or dual-approver reconciliations may help.

-

Repeated Issues Across Reviews

When the same concerns arise year after year, such as payroll discrepancies or last-minute adjustments, it’s time to rethink your control environment.

-

Single-Person Dependency

While cost-effective, depending on one person for all accounting functions poses a serious risk. Bringing in a secondary reviewer or part-time bookkeeper adds a necessary layer of security.

Conclusion: Strengthen Your Internal Controls Before Issues Arise

Weak internal controls can undermine the financial stability of your business, even if you’re growing rapidly. If review engagements consistently reveal recurring issues, it may be time to take a closer look at how your business manages approvals, documentation, and reconciliations.

Whether you’re a startup or a well-established business, investing in strong internal controls is not optional—it’s a strategic imperative for protecting your financial health.

Need support in evaluating your internal controls or preparing for a CPA review?

Contact G&S Accountancy today to learn how we can help identify weaknesses and implement best practices to secure your business’s future.

Frequently Asked Questions (FAQs)

Do I have to implement changes the CPA suggests during a review?

No, but disregarding recommendations—especially those related to internal controls—can increase the risk of errors or fraud and may affect stakeholder confidence.

Is a review engagement a reliable way to assess internal controls?

While not designed to evaluate internal controls explicitly, a review can still reveal control-related red flags through financial analysis and management discussions.

Does a CPA provide a formal report on internal controls during a review?

Not typically. However, CPAs may still share observations or informal suggestions if control issues come to their attention.