Financial Statement Review Problems? Here’s How to Avoid the Most Common Ones

A well-executed financial statement review provides you and your stakeholders with limited assurance that your financial numbers are accurate. Even though this process is less intensive than a full audit, common snags can delay or derail your review. Below, you’ll discover six frequent pitfalls that often obstruct a smooth review engagement, along with practical tips to keep everything on track—written in second-person form to help you prepare effectively.

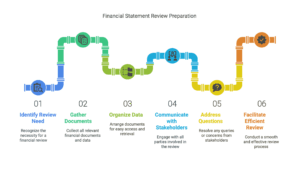

1. Missing or Disorganized Documentation

The Problem:

When your CPA requests bank statements, ledgers, or invoices, but you only have incomplete or disorganized records, your review can stall. Not only does this extend the timeline, but it also raises concerns about your internal controls.

How to Avoid It:

- Develop a straightforward system (digital or physical) for storing all financial documents.

- Use a provided-by-client (PBC) checklist as a roadmap, and gather everything on that list before your CPA begins.

- Reconcile accounts monthly and maintain consistent organization so you don’t scramble at year-end.

2. Lack of Timely Account Reconciliations

The Problem:

If your bank, credit card, or inventory accounts haven’t been reconciled in a timely manner, you’re likely to face unexplained variances. When your CPA notices mismatched balances, it can lead to additional questions and a time-consuming search for errors.

How to Avoid It:

- Reconcile major accounts every month.

- Assign specific team members to conduct and review these reconciliations.

- Investigate and resolve any discrepancies immediately, rather than letting them accumulate.

3. Unrecorded or Inaccurately Recorded Accruals

The Problem:

Expenses you’ve incurred but haven’t paid—or revenue you’ve earned but haven’t billed—may go unrecorded, skewing your financials. Large accrual adjustments during a review can be a red flag for your CPA.

How to Avoid It:

- Keep a running tally of accrued expenses or payables.

- Ensure you have proper cutoff procedures so income is recognized in the correct period.

- Review your accrual entries before handing over your trial balance to the CPA.

4. Incomplete or Insufficient Disclosures

The Problem:

Even in a review (often aligned with GAAP), your financial statements should still include required disclosures—such as related-party transactions or key accounting policies. Omissions can undermine the credibility of your statements.

How to Avoid It:

- Familiarize yourself with your industry’s standard disclosure requirements.

- Maintain a checklist of prior footnotes and update them for any current-year changes.

- Let your CPA know about unusual transactions or shifts in accounting methods early in the process.

5. Major Last-Minute Adjustments or “Surprises”

The Problem:

Your CPA might see late, significant journal entries as a sign that your numbers aren’t reliable, triggering extra scrutiny and prolonging the review.

How to Avoid It:

- Perform regular internal reviews of your financials throughout the year and address issues as they arise.

- Document any substantial adjustments with supporting evidence and logical explanations.

- Eliminate last-minute surprises by planning periodic “mini-closes” well ahead of the official review date.

6. Minimal Communication with the CPA

The Problem:

When management is slow to respond to questions—or fails to mention events like acquiring new debt or making a major purchase—it can appear as if bigger issues are lurking beneath the surface.

How to Avoid It:

- Appoint one person to promptly answer questions from your CPA.

- Schedule regular check-ins to discuss any large upcoming transactions or policy changes.

- Share significant developments (such as equipment purchases or legal matters) the moment they happen.

Tips for a Smooth Review

- Plan Ahead: Know when the review is scheduled and ensure your internal deadlines (for closing the books, reconciling accounts, etc.) are met.

- Use Tools & Tech: Cloud accounting software, collaboration tools, and shared folders can speed up document exchange.

- Stay Organized: Good record keeping is your best defense against all six issues above.

- Ask Questions: Unsure about a new accounting rule or how to treat a specific transaction? Proactively ask the CPA.

Conclusion

By proactively addressing these six pitfalls, you can move through your financial statement review with greater confidence and fewer headaches. Consistent organization, timely reconciliations, and open lines of communication with your CPA go a long way toward producing a clear financial picture.

Ready to streamline your financial statement review? Contact G&S Accountancy today. We’ll guide you through best practices, help organize your documentation, and ensure your review engagement enhances confidence in your company’s numbers.

Frequently Asked Questions (FAQs)

How is a financial statement review different from an audit?

A review offers limited assurance and primarily consists of inquiry and analytical procedures. An audit, on the other hand, provides reasonable assurance through more in-depth testing and verification of financial transactions.

Why are monthly reconciliations crucial for a smooth review?

Monthly reconciliations help you quickly spot and resolve discrepancies before they accumulate. This proactive approach reduces the likelihood of unwelcome surprises and speeds up the review process.

What are some essential disclosures for GAAP compliance?

Common disclosures include related-party transactions, accounting policies, subsequent events, and contingency information. Industry-specific requirements may also apply.

Can G&S Accountancy help me prepare for my next financial statement review?

Absolutely. G&S Accountancy specializes in helping businesses of all sizes get organized, manage accruals, and complete all required disclosures. By partnering with us, you ensure your review goes more smoothly and yields reliable financial statements.