Why Independence Should Matter to You in CPA Reviewed Financial Statements

When you request CPA reviewed financial statements, you’re not merely checking a compliance box—you’re securing third-party validation that can unlock bank financing, grants, and strategic partnerships. That validation only carries weight when the CPA is demonstrably independent. Below, you’ll learn exactly what independence means under SSARS, why it matters so much to every stakeholder, and how you can keep your review conflict-free.

1. The Two Pillars of CPA Independence

Even seasoned executives sometimes blur the line between objectivity and convenience. Remember: independence faces a dual test, and failing either one taints the entire engagement—no matter how meticulous the fieldwork.

- Independence in Fact – Your CPA must be completely free of financial or managerial ties that could even subtly influence their judgment, ensuring their conclusions rest solely on the evidence.

- Independence in Appearance – A well-informed outsider should also see the CPA as neutral; if a reasonable third party could perceive bias, independence is considered impaired.

2. Why Independence Is Crucial in a Review Engagement

Stakeholders treat CPA reviewed financial statements as the middle ground between internal numbers and a full audit—but that middle ground collapses if independence is compromised.

- Lenders: Banks lean on your CPA’s limited assurance to size up credit risk; an independence breach can nullify covenant language and freeze your access to credit overnight.

- Investors & Grantors: Venture capitalists, private-equity partners, and foundations won’t release funds until an unbiased professional verifies your numbers line up with reality.

- Boards & Owners: Independent reviews surface operational or accounting issues that management might overlook—or prefer not to disclose—helping governance bodies fulfill their fiduciary duties.

3. Common Threats to Independence

Conflicts often sneak in through day-to-day convenience—“Sure, the same firm can handle that, too.” Not always.

| Threat | What It Looks Like in Practice |

| Self-review | The CPA firm compiles your books each month and reviews those same numbers at year-end, essentially grading its own homework. |

| Advocacy | Your CPA negotiates a debt workout on your behalf, then turns around and reviews the financial statements affected by that negotiation. |

| Familiarity | A senior partner at the firm is a close relative of your CFO, raising questions about impartiality. |

| Self-interest | The CPA has a significant outstanding loan or other financial stake in your business. |

| Management participation | The CPA makes key accounting decisions—such as determining which costs to capitalize—effectively acting as part of management. |

4. Services That Can Impair Independence

Bundling attest and non-attest services isn’t automatically disqualifying, but you need clear boundaries before adding tasks.

- Tax Return Preparation – Generally acceptable, provided you (not the CPA) choose filing positions and approve all entries, keeping managerial control intact.

- Basic Bookkeeping – Risky territory; independence evaporates if the CPA records transactions or posts adjusting entries without your explicit review and sign-off.

- Financial-Statement Preparation (AR-C 70) – Always impairs independence for reviews because it creates an unmitigable self-review threat; the CPA would be auditing their own work.

- Valuation or M&A Consulting – Proceed with caution; if the valuation feeds directly into the statements under review, independence may be deemed impaired.

- Internal-Control Design – Typically disqualifying because the CPA would later evaluate the very controls they helped craft and implement.

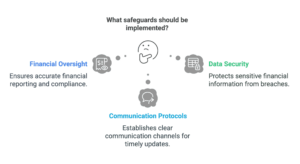

5. Safeguards You and Your CPA Can Implement

A well-designed engagement mitigates risk long before the review report hits stakeholder desks.

- Separate, Detailed Engagement Letters – Use a distinct letter for every service, clarifying scope, management responsibilities, and how independence will be protected.

- Client Oversight & Formal Approval – You sign off on every journal entry, accounting policy decision, and filing position, demonstrating that management—not the CPA—calls the shots.

- Different Personnel or Teams – Assign advisory services and the review engagement to separate staff or even separate offices within the firm whenever possible.

- Periodic Independence Checklists – Have team members complete and a quality-control partner review standardized checklists at each phase of the engagement cycle.

- External Peer Review – Invite an independent firm to review your CPA’s quality-control system and the specific engagement file for an added layer of assurance.

6. Consequences When Independence Fails

One impairment can send shockwaves through your entire financial ecosystem, affecting both compliance and credibility.

- Modified Review Report: The CPA must explicitly state, “We are not independent with respect to XYZ Company,” and many lenders will decline that report outright.

- Loan Covenant Violations: Loss of independence may trigger default clauses, leading to penalty interest rates or immediate repayment demands.

- Grant & Regulatory Risk: Nonprofits can lose critical funding or face adverse audit findings that jeopardize future awards.

- Reputational Damage: Stakeholders begin to question management’s transparency and governance, potentially raising the cost of future capital.

7. Your Action Plan to Protect Independence

Independence is a shared responsibility—take these steps to keep your review conflict-free.

- Map Your Service Needs: List every bookkeeping, tax, advisory, and attest task you expect over the next 12–18 months so you can spot overlaps early.

- Assess Independence Early: Discuss potential conflicts with your CPA before year-end, when there’s still time to restructure work or bring in a second firm.

- Document Every Management Decision: Maintain evidence—email trails, approval logs, board minutes—showing that final judgments rest with management.

- Bring in a Second Firm for High-Risk Projects: For mergers, complex valuations, or major system implementations, engage specialists who won’t compromise the reviewer’s impartiality.

Conclusion

Independence isn’t bureaucratic red tape; it’s the trust framework that transforms CPA reviewed financial statements into decision-ready documents for bankers, investors, grantors, and boards. Respect the rules and you’ll protect your access to capital while elevating your organization’s credibility.

Have questions about your current service mix? Contact G&S Accountancy Inc. or send an email at info@gns-cpas.com. We’ll guide you through an independence assessment and design a service structure that keeps you compliant and efficient.

Frequently Asked Questions

Can the same CPA firm that prepares my tax return also issue my CPA reviewed financial statements?

Often yes—if you, not the CPA, make all tax-related decisions and the firm documents safeguards that eliminate any self-review or management-participation threats. When in doubt, request an independence worksheet before the review starts.

What’s the main difference between compiled, reviewed, and audited statements?

A compilation offers no assurance, a review provides limited assurance that your financials are free of material misstatements, and an audit supplies reasonable (higher) assurance. If lenders or investors ask specifically for CPA reviewed financial statements, an audit or a compilation won’t satisfy them.

How long does a review engagement usually take once I submit my records?

For a well-organized mid-size entity, two to four weeks is typical. Timelines stretch when reconciliations are incomplete, supporting documents are missing, or independence concerns force service reshuffling.

Do privately held companies really need CPA reviewed financial statements?

If you’re seeking bank financing, courting investors, or meeting board or grant-maker requirements, yes. A review provides a cost-effective credibility boost compared with an audit while still reassuring stakeholders that your numbers have been vetted by an independent CPA.

What materials should I gather before the CPA begins the review?

Be ready with a year-end trial balance, bank reconciliations, legal and debt agreements, significant contracts, and explanations of any unusual transactions. Supplying complete documents up front shortens the review timeline and reduces follow-up questions.